I just finished filling out my March Madness brackets (for recreational purposes only, I assure you), so I think we also should start a pool on when the next utility will ask its state regulators for permission to build a new, large-scale nuclear power plant? If we did, should ‘never’ be one of the options?

Anyone willing to put their money on Georgia Power? The company actually had gotten state approval to do some preliminary work at a possible site for two new reactors In Stewart County on the border with Alabama. But earlier this month the utility told regulators it was suspending work on the expansion plans at least until its 2019 integrated resource plan is filed.

How about Florida Power & Light? The company’s planned two-unit expansion at Turkey Point has been on the books since 2008, when FPL was optimistically forecasting the new reactors would be up and running by 2018 and 2020, before subsequently pushing the start-up back first to 2022 and 2023 and now to 2027 and 2028. But last year the company told Florida regulators that while it still intended to secure its NRC license for the facility (which is expected sometime this year), it didn’t intend to do anything else until 2020.

Finally, how about Dominion Resources, which has been pushing for years to add a third unit to its North Anna site in Louisa County, Va. The proposed reactor, a 1,470 MW design developed by GE and Hitachi known as the ESBWR (Economic Simplified Boiling Water Reactor), is a first-of-its-kind unit with an estimated capital cost of almost $15 billion and an all-in cost of about $20 billion. Despite its enthusiasm for the project, even Dominion acknowledged in its 2016 IRP that the reactor was only economic in one scenario—full implementation of the former Obama administration’s soon-to-be defunct Clean Power Plan.

The problems for these companies, and any others considering such a step, go well beyond the well-documented, and still far-from-over cost overruns and delays that have plagued the four new reactors currently under construction in Georgia and South Carolina. The real issue is that the technology—one with high capital costs requiring a long time of steady state operation to get into the black—doesn’t mesh with the nation’s rapidly evolving electric power system. Committing to a nuclear plant constrains you for at least 40 years, and perhaps for as long as 80 years; and while you are still committed, everything else is changing.

The key change in the last 10 years has been the revolution in natural gas supply made possible by fracking and horizontal drilling. In turn, that has driven natural gas prices down to levels thought impossible just a decade ago—with no reason to think sharp increases are anywhere in the future.

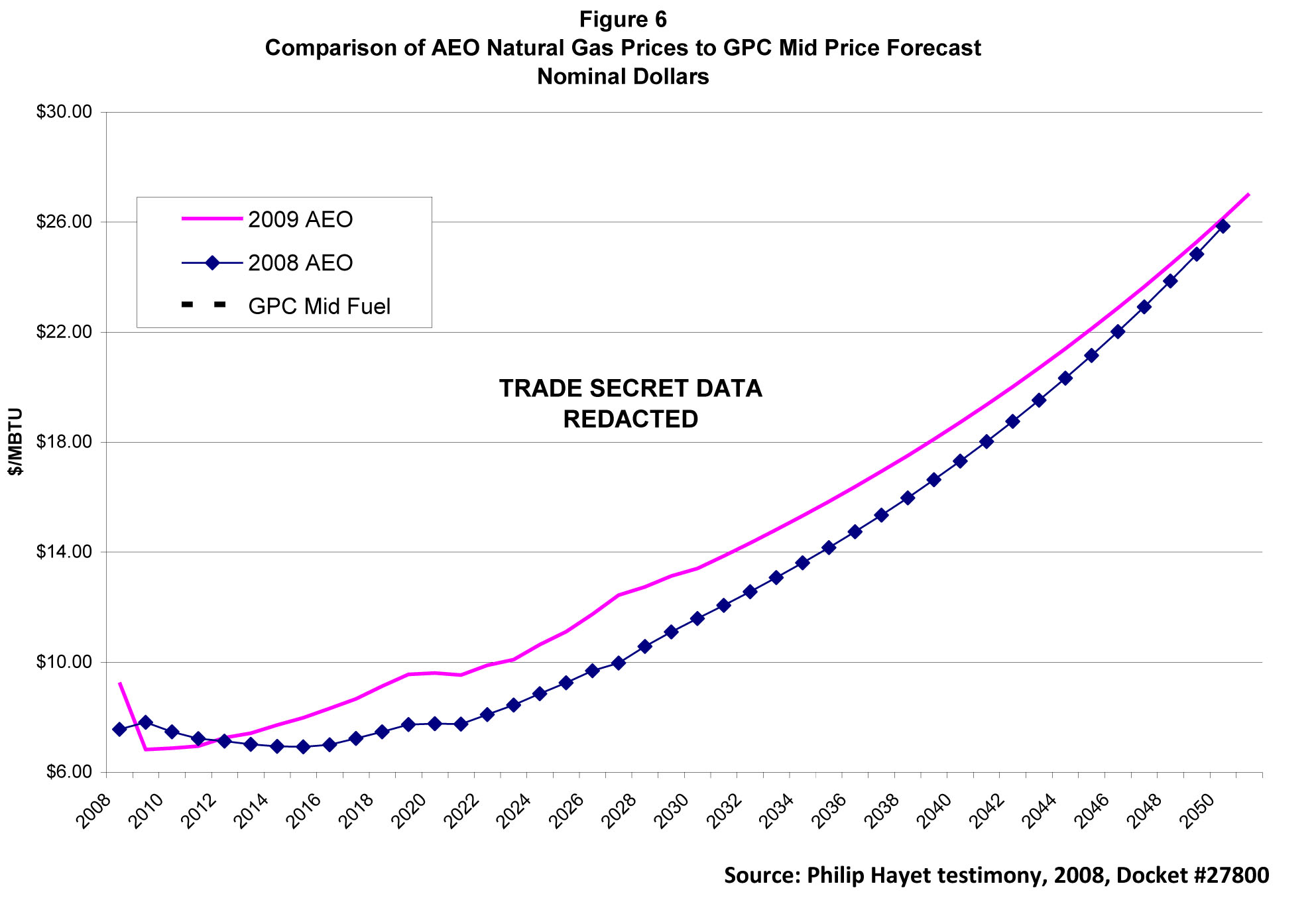

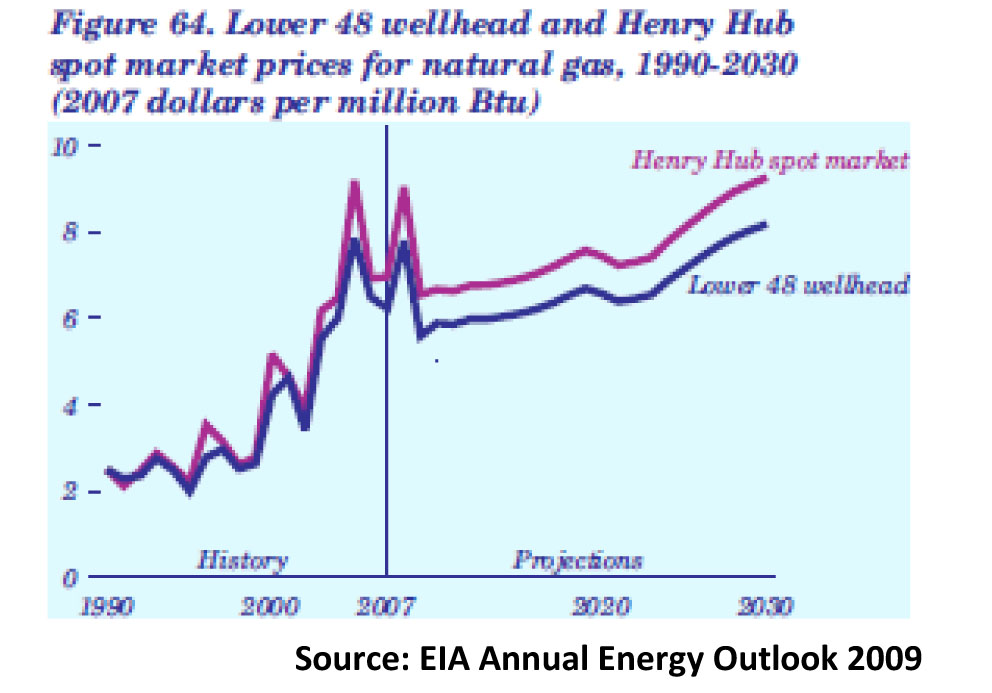

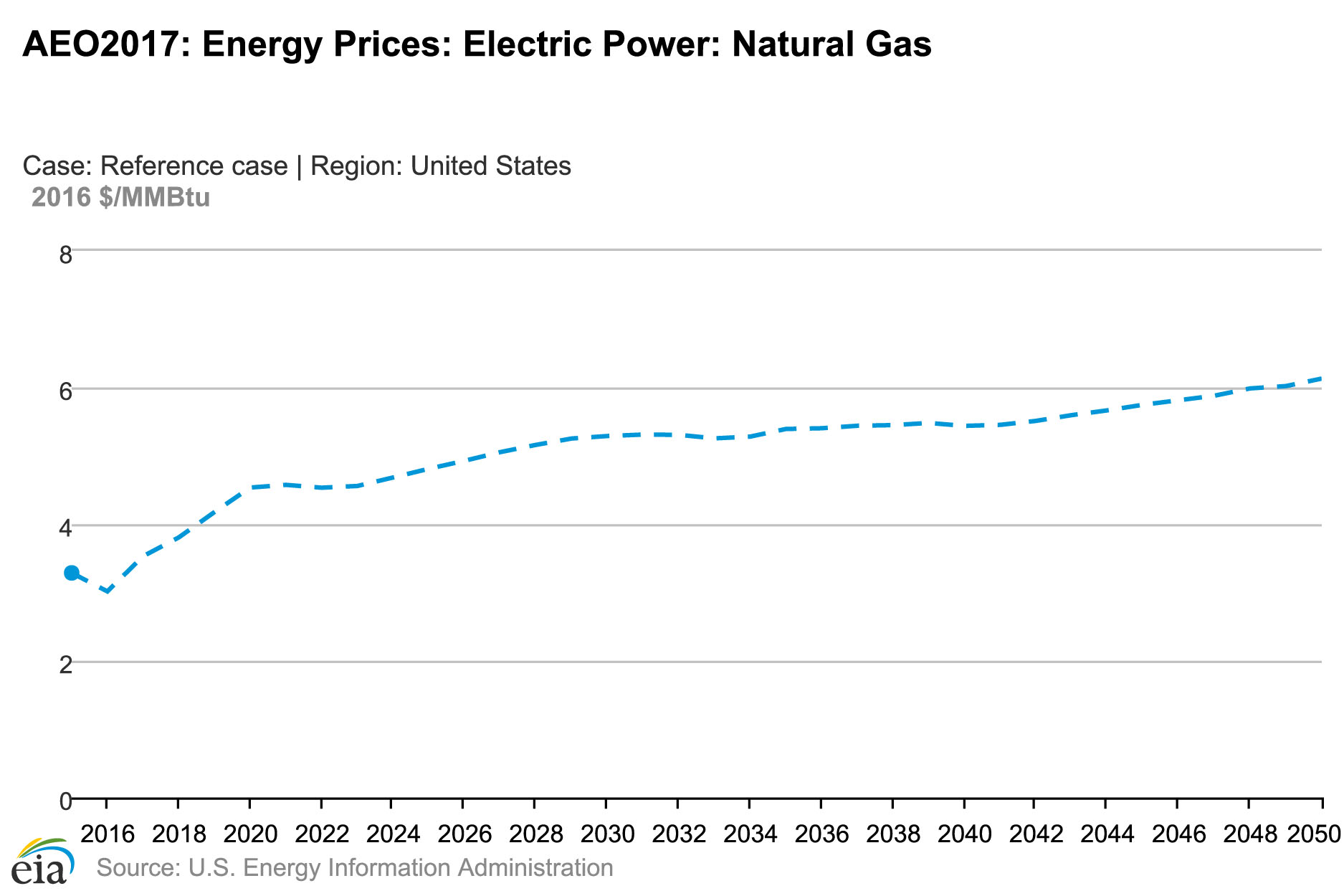

During the review process for Georgia Power’s Vogtle 3&4 plants, the company and other witnesses presented forecasts from the Energy Information Administration (as well as its own, but more on that in a minute) that look almost laughable today. Take a look at the chart below—prices never drop below $6 per million British thermal units and spend most of the forecast period well above $10 per mmBtu. Now that forecast was in nominal dollars, but even an inflation-adjusted view (see the second chart) has the prices well above $6 per mmBtu for the duration. Compare that to EIA’s 2017 forecast (the third chart), which keeps gas prices below $6 per mmBtu (in 2016 dollars) through 2050.

This radically different outlook for natural gas prices is crucial—since at current levels the Vogtle plants may never make it into the black. In his 2008 testimony during the Vogtle 3&4 certification process before the Georgia Public Service Commission, Philip Hayet, testifying for the commission’s public interest advocacy staff, warned repeatedly that under a low natural gas price outlook the economics of the Vogtle expansion didn’t make sense.

The most telling portion of his testimony follows below. As you can see, portions of his testimony have been redacted (those sections with XXXXX), which was done at Georgia Power’s request. This is a frustrating process for an outside observer since it prevents a complete evaluation of the material for no apparent reason. It is as if state secrets were involved and letting everyone know would somehow compromise the company; instead of, as I would argue, improving the decision-making process by broadly disseminating all available information. That aside, it is fairly easy to fill in the blanks through a careful reading of the testimony, as I have suggested below, particularly when you consider the two paragraphs together.

“In Figure 11 [also redacted, as are all of the graphics with Georgia Power information in them], the one case that is uneconomic over the entire study period is XXXXXXX XXXXXXXXXXX [low natural gas prices and no carbon dioxide tax/fee]. In that potential future outcome, the nuclear unit will have been a XXXX [I will let you fill in your preferred adjective here, but clearly he means the reactors would have been a bad economic decision]; however, nobody in the utility industry believes that this case is feasible, as there is a great expectation that there will be XXXXX [a CO2 tax/fee] of some form. In the highly unlikely event that XXXXXXXX [no fees/taxes] are imposed, there would most likely be significant gas fired generation built. That in and of itself would be the cause of driving up natural gas prices.

“Excluding the low fuel, no CO2 scenario, which I discussed above, each of the other cases appear uneconomic for some time period before turning up and moving into positive territory.”

I added the emphasis above, since that is clearly where we are today—and could be for the life of the new Vogtle reactors. I cannot say what the ‘low natural gas price’ was that Georgia Power used in its analysis, but remember that at the time prices were never expected to drop below $6 per mmBtu, and notice that even though Georgia Power’s data is redacted, the chart itself starts at $6 per mmBtu and moves up from there. Clearly if its forecasts were below that level the y axis would have had a different starting point.

At a subsequent point in his testimony, Hayet said: “The conclusion that I reach once again is that the benefits of Vogtle 3 and 4 will be greatly tied to what happens to natural gas and CO2 costs in the future, which no one knows for sure. “

That is precisely the problem for any new large nuclear power projects—they commit you to a future you can’t predict.

The inability to predict the future is also evident in the rapid generation technology changes that have occurred since FPL began pushing its new nuclear plans. In 2008 there were perhaps 800 MW of installed solar photovoltaic capacity nationwide; since then almost 40 gigawatts of PV capacity have been installed. And that is just the beginning: The latest GTM Research-SEIA solar market report projects that roughly 85 GW of new solar will be installed in the next six years.

Interestingly, one of the places where solar finally is beginning to take hold is in the Sunshine State, where FPL recently has moved forward with a significant expansion of its solar capacity. The utility brought three new facilities, totaling 223.5 MW of PV capacity, online at the end of 2016, and by the end of February had announced plans to build another eight plants, at 74.5 MW each for a total of 596 MW, by early 2018. In contrast, in its 2008 10-year planning document, the first filed after it began the process to build its two new reactors at Turkey Point, the utility noted that its Rothenbach Park solar facility, completed in October 2007, was then the largest plant in the state “and one of the largest in the southeastern United States.” Its total generating capacity was just 250 kilowatts.

Clearly, here too, much has changed, and that brings us right back to the commitment issue. Once committed to a 40- or 60-year nuclear operating lifespan, which at least at this point FPL still is not, shifting gears to embrace a new technology—one that is emissions free and cost competitive—is difficult, if not impossible.

Finally, there is the incompatibility of the long lead times required for large nuclear power plants and the assumptions made during the planning process concerning load growth. For example, in its 2008 10-year plan cited previously, FPL projected that residential demand (which accounts for the majority of the utility’s load) would climb from 57,243 gigawatt-hours (gwh) in 2008 to 77,121 gwh in 2017, a whopping 34.7 percent increase. Part of the increase, the utility said, would be due to population growth, but the rest would be attributable to higher per capita consumption—with the utility projecting that average annual usage would climb from 14,174 kilowatt-hours (kwh) per customer to 16,514 kwh.

In its latest 10-year outlook, the 2016-2025 plan submitted last spring, FPL noted that actual residential consumption in 2015 totaled 58,846 gwh, an average of only 13,920 kwh per customer. Looking ahead, the utility said, the downward trend in per capita consumption is almost certain to continue; it projected that by 2025 average residential usage will have dropped to 12,516 kwh annually. [The 2008 10-year plan can be found here; the 2016 plan can be found here.]

The impact of the LED revolution and the various appliance efficiency standards implemented recently (particularly those regarding heat pumps and air conditioning units) can clearly be seen in these estimates. I certainly don’t blame FPL for its forecasts, 10 years ago the number of LEDs installed in the U.S. was essentially zero, but that brings us back to the problem of committing to a technology with such long lead times (and then such long operating horizons). In our rapidly changing energy environment, those commitments are a real problem.

Some of these issues could be addressed with strong leadership from Washington. For example, a carbon tax certainly would help to change the equation, particularly if it was high enough to take a real bite out of competing fuels such as coal and natural gas. But given the current administration’s hoax-based approach to global warming (and the general unease within the Republican Party to doing anything other than to lower taxes), I do not see support for such action coming from the capital in the coming four years.

My pool pick? The fat lady wins, new large-scale nuclear power plants are headed to the losers’ bracket.

–Dennis Wamsted

Follow

Follow

Dennis, whatever you do don’t put your money on Watts Bar 2, which came online in 2016 and is now generating more clean electricity than all solar east of the Mississippi. At a lower cost, and taking up a lot less room.

In TVA territory, you’ll even be able to blog about renewables at night – not that people will care much longer.